Time management is very much important in IIT JAM. The eduncle test series for IIT JAM Mathematical Statistics helped me a lot in this portion. I am very thankful to the test series I bought from eduncle.

Nilanjan Bhowmick AIR 3, CSIR NET (Earth Science)

- UGC NET

- Commerce

How to learn this formulas is there any trick and is mai sai kasi ques ban kar aa saktai hai

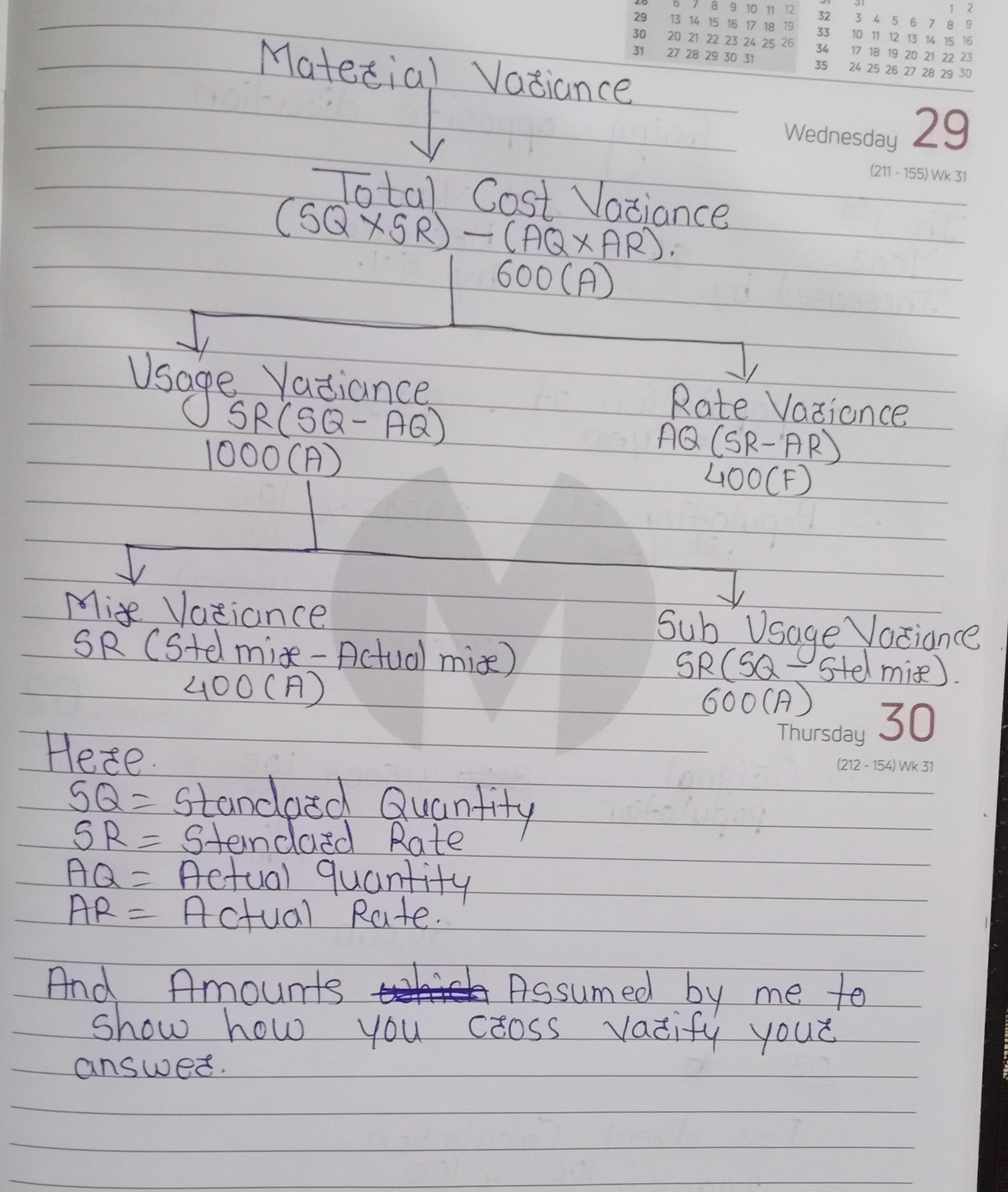

EEOUcie.co Change1n mater1als purchase, upkeep, and store-keeping cost. (This is an are allocated to direct material costs on a predetermined Or Standard cost applicaIC Only when such eh Eduncle.c .com Change in qualiy or specitication or marerial plurcnasel cost basis.) aterial yield varian = (Standtard Use of substitute material having a higner or lower unit pruCe ed for Acul Ma o sned by dividing ht Votak ca (Standard yield pri total quanuty (numk by d number of physica by the total qua Direct Materials Usage Variance: The difterence between tne actual quantity us Price) the actual quany used and the amount which Cnange 1n the pattern or amounts of laxes and duues. al unissy sOSP (Standard Price x Act Quantity have been used, valued at standard pice Standard Quantity for actual output x Standard Direct materials usage variance SOxSP) - GPx 90) Standard Quantity for A = SQSP-AQSP or SQ where, cual Production ox Outpuat Standard Price = Standard Price x (Standard Quantity for actual output - Actual Quantity) SP Actual nantity of Material Consumed SP (SQ-A) AQ AP = Actual Price RSQ = Revised Standard Quantity Causes of Materials Usage Variance als. Variation in usage of materials due to Inetticient or careless use, or econor . sOSP = Standard Cost of Stand. Change in specification or design of product. . Matenal RSQSP = Revised Standard Cost ot Standard Material C. Inefticient and inadequate inspecion of raw materials AQSP = Standard cost of Actual Material Purchase of inferior materials or change in quality of materials 1. Actual Cost of Actual Material AQAP = Rigid technical specifications and strict 1nspection leading to more rejections which reani als . aterial Sub-Usage or Yield Variance rectification. (a) Material Mix Variance = 12 sa sP -sssP (b) Inetficiency in production resulting in wastages (C) Material Usage Variance 2-3 Use of substitute materials. (d) Material Price Variance = 1-3 . Theft or pilferage of materials. (e) Material Cost Variance 34 Inefficient labour force leading to excessive utilisation of materials. ading to breakdowns 14 and mote Defective machines, tools, and equipments, and bad or improper maintenance leading to hra cet Variance: Direct LabOur Cost Variance (also temed Direct Wage Variance) is the ditierence usage of materials. 3. Direct Labour Cost Varianc direct wages incurrea and he standard direct wages specified for the activiny achieved. Yield from materials in excess of or less than that proVIded as the standard yield. between the actual direct be wasted while being use ate Variance (Wage Rate Variance): The difference between the actual and standard wage roa k. 1. Direct Labour per hour applied to the total hours worked. Wages rate riance Standard Rate - Actual Rate) x Faulty materials processing. Timber, for example, if not properly seasoned may be wasted wh: in subsequent prOcesses. are no Accounting errors, e.g. when materials returned from shop or transferred irom one job to anotha m. = (SR-AR) x AH properly accounted for. Inaccurate standards SRAH- ARAH Change in composition of a mixture of materials for a specified output. 0. Causes of Direct Labour Rate Variances Change in basic wage strueture or Cnange in piece-work rate. These will give rise to a varnance till suc mpostion a. i) Direct Materials Mix Variance: One of the reasons for materials usage variance is the change in the comnosit. the standards are not revised. of the materials mix. The difference between the actual quantity of material used and the standard proportion, ni Emplovment of workers of grades and rates of pay different from those specified, due to shortage o at standard price. b. of the proper category, or through mistake, or due to retention of surplus labour. Mix variance = (Revised Standard Quantity Actual Quantity Standard Price. Payment of guaranteed wages to woTKers wno are unable to earn their normal wages if such guarant = RSQSP-AQSP form part of direct labour cost. Use of a different method of payment, e.g. payment at day-rates while standards are based or ii) Direct Materials Yield Variance: Yield variance is the difference between the standard cost of producion achieved and the actual total quantity of materials used, multiplied by the standard weighted average price per un method of remuneration. Contact Us: Website : www.eduncle.com Email: support@eduncle.com Call Us: 7665435300 Contact Us: Website: www.eduncle.com Email : support@eduncle.com Call Us:7665435300

1 Answer(s)

Answer Now

- 0 Likes

- 2 Comments

- 0 Shares

Do You Want Better RANK in Your Exam?

Start Your Preparations with Eduncle’s FREE Study Material

- Updated Syllabus, Paper Pattern & Full Exam Details

- Sample Theory of Most Important Topic

- Model Test Paper with Detailed Solutions

- Last 5 Years Question Papers & Answers

Sign Up to Download FREE Study Material Worth Rs. 500/-

Gunjan

or iski koi vedio hai